May 4, 2026

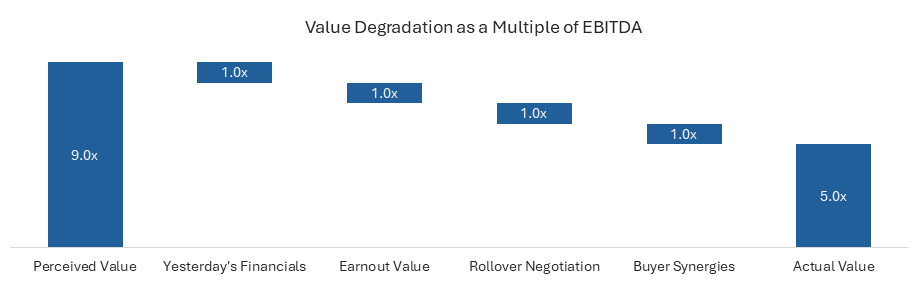

How a “9x” Deal Quietly Becomes a “5x” Outcome, One Turn at a Time

Valuation multiples are one of the most commonly discussed topics among owners in community association management. Whether the conversation begins with a recent transaction, inbound buyer interest, or a peer who recently sold, the discussion often gets distilled down to a single number. “My friend sold for 9x.” “We are probably an 8x business.” “A buyer already told us we are worth 9x.” There is nothing inherently wrong with these conversations, and in many cases the headline multiple itself may be directionally accurate. The problem is that headline multiples, by themselves, rarely tell the full economic story.

In practice, a business that “sells for 9x” can still feel like a 9x outcome to the seller all the way through closing. The letter of intent may say 9x. The purchase agreement may still support 9x. The congratulatory conversations after the deal may still center around 9x. The problem is that, beneath the headline, the buyer may be economically underwriting something much closer to 5x. Not because the buyer openly reduced the valuation, and not because the seller necessarily negotiated poorly. More often, value simply leaks out over the course of the process, one turn here, another turn there, through timing, structure, valuation methodology, and economics that are often far less visible than the headline multiple itself. By the end, the multiple may still say 9x. The buyer often knows otherwise.

Here is how it happens.

Turn One, Selling Off Yesterday’s Financials

The first turn often disappears before the letter of intent is even signed. Many owners enter a sale process using trailing financial statements that are already one or two months behind current operations. On the surface, that feels entirely reasonable. After all, those are the latest completed financials, they tie cleanly to the accounting records, and they are what most buyers initially request.

The problem is that community association management businesses are rarely standing still. If EBITDA is growing annually, and a transaction process takes months from initial outreach to closing, the business that exists at close may be materially different from the business reflected in the financials that originally anchored the valuation discussion. By the time legal documentation is being finalized, the seller may have already created a meaningful amount of incremental EBITDA that is simply not being reflected in the economics of the transaction.

This is where many owners unintentionally give away a turn. At the beginning of a process, both buyer and seller are effectively estimating what the business will look like months in the future. The question is not what EBITDA looked like two months ago. The question is what EBITDA the buyer will actually inherit on the day the transaction closes.

In many cases, that forward EBITDA, supported by a credible corporate budget and validated through monthly execution during the process, may be the most economically relevant earnings figure in the entire transaction.

Sophisticated buyers understand this. Sellers should too. Owners who allow the valuation discussion to remain anchored to stale trailing financials, rather than the EBITDA the buyer is actually acquiring at close, often give away value before negotiations even begin.

Turn Two, The Earnout That Preserves the Headline, But Not the Economics

The second turn often disappears through structure. Earnouts are frequently presented as a clean way to bridge valuation gaps while allowing both sides to “meet in the middle.” On paper, they can preserve the headline multiple and make both sides feel aligned. A buyer may say, “We are still paying your number, part of it is simply tied to performance.”

That sounds reasonable.

The reality is that the earnout money has to come from somewhere. Whether the earnout is technically being paid by the acquired company, a holding company, or a larger parent platform, the dollars do not appear out of thin air. They come from the cash flows of the business being operated after closing.

This becomes even more important when rollover equity is involved. Regardless of whether the acquired company or the parent platform is funding the earnout, the rollover seller already owns a portion of that economic engine. In other words, part of the cash being used to fund the earnout may already be partially owned by the seller themselves.

The higher the rollover percentage, the more economically circular the arrangement can become.

On paper, the multiple may still say 9x.

Economically, the buyer may already be underwriting something materially lower.

We explored this dynamic in greater detail in our earlier article on earnout structures.

Turn Three, Rollover Equity Negotiated in Dollars Instead of Ownership

The third turn often disappears in rollover equity. Most owners naturally focus on the dollar value of their rollover. “I am rolling $5 million.” “I am keeping $10 million in equity.” Those numbers sound meaningful, and in absolute terms they are. The problem is that rollover negotiations are rarely about dollars. They are about ownership.

Behind every rollover discussion is a much more important question: what percentage of the buyer’s platform will the seller actually own at closing, and how much of the next liquidity event will that ownership ultimately participate in? This is where many sellers unintentionally think about the economics backwards.

The platform share value presented by the buyer is often a negotiated paper number. And when the seller’s rollover amount is fixed in dollars, that paper number directly determines how many shares the seller receives at closing. A higher implied platform share value means fewer shares issued to the rollover seller. A lower implied platform share value means more shares issued to the rollover seller for the exact same rollover dollars.

In other words, what many sellers initially perceive as “more valuable” can often result in less ownership. And less ownership can mean less participation in future upside, less influence over eventual liquidity outcomes, and less exposure to the very value creation that made the rollover attractive in the first place.

Buyers understand this math extremely well. Owners who negotiate rollover equity based primarily on dollar value, rather than ownership percentage and long-term economics, often give away another turn without realizing it.

Turn Four, Giving Buyer Synergies Away for Free

The fourth turn often disappears after the buyer already knows exactly where the upside is. Experienced acquirers in community association management understand vendor purchasing leverage. They understand insurance purchasing leverage. They understand technology consolidation. They understand regional density. They understand shared overhead. In many cases, they have already built underwriting models around these synergies before the seller even enters the process.

What many owners do not fully appreciate is that these synergies have real economic value, and buyers are often willing to pay based not only on the value the business generates on a standalone basis, but on the value they believe they can create after closing through integration. That does not mean every synergy should belong to the seller. But it also does not mean every synergy should automatically belong to the buyer.

The challenge is that sellers often cannot fully identify, quantify, or monetize these synergies on their own. Much of that value exists inside the buyer’s underwriting model, not the seller’s operating model. This is one of the areas where an experienced sell-side advisor can materially change the economics of a process, not simply by identifying where strategic value may exist, but by helping translate that value into competitive buyer behavior.

Just as importantly, buyers rarely volunteer to share synergy value in a one-on-one negotiation.

They often do in a competitive process.

When multiple qualified buyers understand that an asset is being actively pursued by other credible bidders, their willingness to pay often increases naturally. In many cases, buyers begin sharing more of the post-close value they expect to create, not because they suddenly view the asset differently, but because the competitive dynamics of the process require it.

The Headline Multiple Is Easy to Share. The Structure Usually Is Not.

This is why owners should be cautious when comparing multiples with peers. When an owner says, “My friend sold for 9x,” what usually gets shared is the headline. What rarely gets shared is whether the valuation was based on trailing financials that were already stale, how much of the consideration was contingent, who set the value of the rollover shares, how much buyer synergy was transferred without negotiation, or how much of the “purchase price” was actually funded by cash flows the seller continued helping create after closing.

By the time those details surface, the seller may still believe they sold for 9x.

The buyer may know they purchased something much closer to 5x.

Subscribe to our newsletter!

Get the latest industry insights and market updates from CAM Advisors.