August 11, 2025

Earnouts: The Hidden Valuation Trap That Can Quietly Cost Sellers Millions

For many business owners in their late 40s, 50s, and 60s, the sale of a business is not just a transaction. It is the final chapter of decades of early mornings, long nights, calculated risks, and personal sacrifice. That is why it can be so frustrating to think you have negotiated a strong price, only to find out later that the deal was worth far less than you thought.

One of the biggest culprits in this kind of disappointment is the earnout. Buyers often use earnouts to make a purchase price look higher than it truly is. This is not inherently bad. In some situations, an earnout can help bridge a valuation gap and increase total proceeds. But sellers need to be very careful in how they evaluate them.

This article will walk you through what an earnout really means, the different ways it can be paid, and how to properly discount its value. We will use a real-world style example so you can see exactly how a “10.0x” multiple can turn into an 8.6x multiple once the dust settles.

What is an Earnout?

An earnout is a contractual agreement in which a portion of the purchase price is paid later, contingent on the business hitting specific performance targets after the sale. These targets might be revenue milestones, EBITDA levels, customer retention goals, or other operational benchmarks.

Earnouts are appealing to buyers because they reduce risk. Instead of paying you everything upfront, the buyer only pays the remaining amount if the business performs well under their ownership.

For sellers, earnouts can sometimes boost the headline price, but they also introduce uncertainty. Hitting the targets may be harder than expected, especially if you have less control after closing. And even if you hit them, the way the earnout is paid matters a great deal to your true proceeds.

The Example: How a 10.0x Deal Shrinks in Value

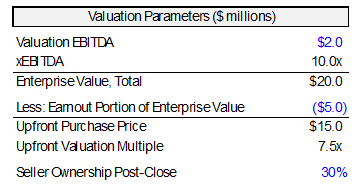

Imagine you are selling a company that generates $2.0 million of EBITDA. A buyer offers a 10.0x multiple, which works out to a $20.0 million enterprise value. It sounds like a strong price. However, only $15.0 million will be paid upfront at closing. The other $5.0 million will be structured as an earnout, payable in 2 years if the company meets agreed-upon performance goals. You also agree to roll over 30% ownership into the new entity, meaning you will still own a minority stake in the business post-closing.

At first glance, this still looks like a $20.0 million deal. Many sellers would mentally add the $5.0 million earnout to the $15.0 million upfront payment and call it a day. But there are two major adjustments that need to be made to see the true value you are getting.

Step 1: Who is Paying the Earnout?

Earnouts can be paid either by the buyer’s holding company or by the operating business itself. In this example, the earnout is being paid by the business 2 years after closing. Because you own 30% of that business, 30% of the cash used to pay the earnout is effectively coming out of your own pocket.

If the earnout is $5.0 million, that means only 70%, or $3.5 million, is truly being paid by the buyer. The rest is simply moving from one of your pockets to another.

Step 2: Discounting the Earnout

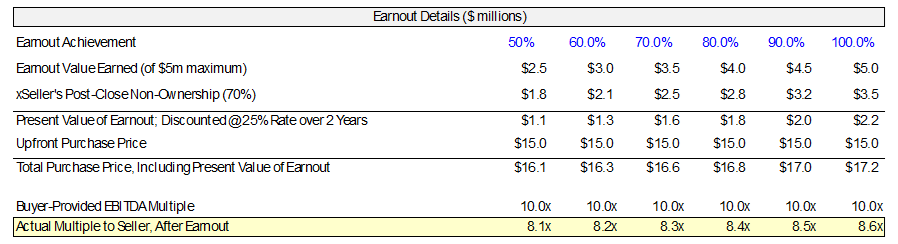

Even if you are confident the earnout will be achieved, future money is worth less than money today. That is why the earnout needs to be discounted back to its present value. Using a 25% annual equity discount rate, a maximum $5.0 million received in 2 years has a present value of approximately $3.2 million. Because you are only truly receiving 70% of that, your real earnout value in today’s dollars is about $2.2 million.

Step 3: Seeing the Real Price You Are Being Paid

When you add the $15.0 million upfront payment to the $2.2 million present value of the earnout, the actual economic value you are receiving is about $17.2 million. That is a $2.8 million gap between the “headline” figure of $20.0 million and the true proceeds you will put in your pocket. In valuation terms, this means the real multiple being paid for your company is about 8.6x EBITDA, not the 10.0x EBITDA that was promoted in the offer. In the event you earn less than the full value of the earnout, the total upfront multiple will be even less than the 8.6x.

Why This Matters for Sellers Like You

If you are in your 50s or 60s, this sale may be the single largest liquidity event of your life. You may be thinking about retirement, estate planning, or launching a second act as an investor or entrepreneur. The difference between $20.0 million and $17.2 million is not just a rounding error. It can mean millions of dollars in lost investment income over the rest of your life.

It is also about peace of mind. If you are planning to step back from the business after closing, your ability to control the factors that determine whether the earnout is achieved will be much smaller. A buyer could make operational changes that hurt short-term performance, and you could miss the target through no fault of your own.

Key Lessons for Sellers

Always ask who is paying the earnout. If the company is paying it and you own part of that company, you are funding part of it yourself. Always discount future payments using your equity rate of return, not the buyer’s lower cost of debt. Always run the real math on valuation rather than relying on headline multiples that assume full face-value earnouts. And always negotiate accordingly. A smaller guaranteed check today may be worth more than a larger earnout that is uncertain and partly self-funded.

Bottom line: Earnouts are a tool, not a gift. They can work in your favor when structured correctly, but they can just as easily mask a lower true valuation. For business owners, understanding these mechanics before you sign a letter of intent can protect millions of dollars in value and ensure that decades of hard work translate into the financial outcome you deserve.

For more information on the HOA management industry, valuation metrics, or other questions, please email contact@camadvisors.co or visit https://www.camadvisors.co/

Subscribe to our newsletter!

Get the latest industry insights and market updates from CAM Advisors.