April 2, 2026

Insurance as a Revenue Driver for HOA Management Companies

Insurance is one of the most consequential financial decisions made by a homeowners association. Annual premiums are material, liability exposure can be severe, and coverage gaps can create long-term financial risk for both the association and its management company.

What is less commonly understood is that these premiums also contain embedded distribution economics.

In many cases, management companies are directly involved in the insurance process and capture none of that value.

Why Management Companies Sit at the Center of Insurance Decisions

HOA management companies occupy a structurally unique position in the insurance ecosystem.

Most full-service management agreements require associations to maintain specific insurance policies, often with detailed requirements regarding minimum limits and other specific terms. In many agreements, the management company must be included as a definitional insured or additional insured. Performance of management services is frequently conditioned on receipt of compliant certificates and endorsements.

This contractual structure makes insurance procurement inseparable from the management relationship. It also gives management companies operational visibility into renewal cycles, carrier performance, claims patterns, and coverage structure.

Representation and Compensation

In the brokerage model, the broker represents the association but is typically compensated by the carrier whose policy is placed. That compensation is embedded within the premium rather than billed separately.

In the agency model, the agency represents the insurance carrier and is likewise compensated by the carrier through commissions embedded within the premium, which may be shared with producers working on the agency’s behalf.

In both cases, the carrier compensates the intermediary for placing the policy. The intermediary may be either a broker or an agency, depending on the structure. The economics are driven by placement, even though legal representation differs.

As a result, the total commission exists regardless of structure.

This creates a structural economic question: If these economics are embedded in the premium, how are they allocated, and who ultimately captures them?

Illustrative Economics at $5,000,000 of Annual Premium

Assume a portfolio generating $5,000,000 in annual premium across a typical basket of HOA insurance coverage: commercial general liability, directors and officers and employment practices liability, and umbrella coverage.

At a blended commission rate of 12%, the total gross commission pool equals $600,000 per year.

For many management companies, that $600,000 accrues entirely to an external intermediary.

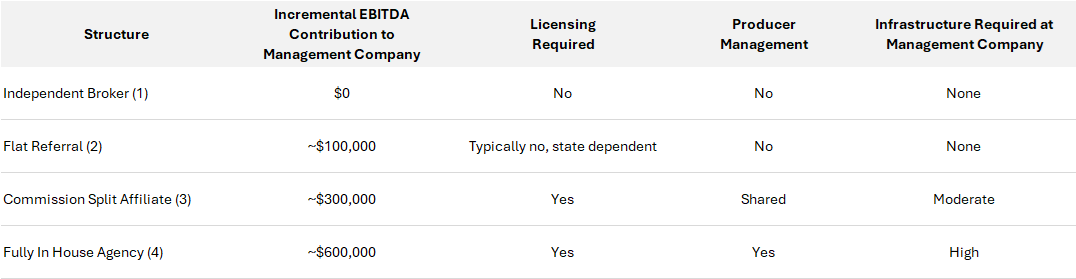

Structural Progression

The allocation of that $600,000 depends entirely on structure.

More specifically, it depends on how the insurance distribution function is organized and how much responsibility the management company is willing to assume within it.

The underlying economics do not change. The premium is paid, and the commission is generated. What changes is who captures the value.

- In an independent broker model, the management company participates operationally but does not participate economically.

- In a referral structure, the management company participates through a limited economic arrangement with minimal additional infrastructure.

- In a commission split affiliate structure, the management company participates more directly in the distribution margin while taking on licensing and coordination requirements.

- In a fully in-house structure, the management company assumes responsibility for licensing, compliance, and execution in exchange for retaining a larger share of the economics.

Across these structures, the total commission pool remains the same, but participation in that pool shifts depending on how the distribution function is structured.

This progression reflects a straightforward trade-off: As execution and internal infrastructure requirements increase, so does economic participation.

Because these policies renew annually, the associated commission streams are typically recurring so long as coverage remains in force. In commercial insurance, retention rates are often high, and renewal commissions are generally consistent with new business commissions.

As a result, insurance distribution revenue tends to exhibit a stable, recurring profile tied to policy renewals rather than to episodic transaction activity.

For management companies, this has an additional implication. To the extent this revenue is tied to a retained portfolio of communities, it is generally consistent with the recurring, contracted nature of the core management business and is not typically dilutive to overall valuation multiples.

Closing

Insurance is often viewed as a required cost within the HOA model.

In practice, it is a recurring economic layer with embedded value.

For management companies, the question is not whether that value exists, but how it is structured, how it is allocated, and what level of responsibility they are willing to assume in order to capture it.

Footnotes

(1) Independent Broker. Assumes $5,000,000 in annual premium and a blended commission rate of 12 percent, resulting in $600,000 of gross commission paid by carriers to the broker. The management company receives no commission participation. EBITDA contribution is therefore $0.

(2) Flat Referral Model. Assumes the broker receives $600,000 in gross commission. The management company is not licensed and therefore cannot receive percentage based commission in most jurisdictions. Compensation is structured as a flat annual referral fee, assumed here to be approximately $100,000. Because this income typically requires minimal incremental cost, it is treated as approximate incremental EBITDA. Actual legality and structure are state specific and require regulatory compliance and disclosure.

(3) Commission Split with Licensed Affiliate. Assumes gross commission of $600,000. In this structure, the management company participates in the distribution economics through a licensed affiliate arrangement. The figure shown reflects the management company’s share of the commission pool prior to any internal compensation to producing personnel or allocation of overhead. Actual realized EBITDA will depend on how producer compensation and cost allocation are structured.

(4) Fully In House Licensed Agency. Assumes gross commission of $600,000 captured within a fully owned and operated agency structure. The figure shown reflects total commission revenue prior to any internal compensation to producers or allocation of operating costs, including licensing, compliance, and infrastructure. Actual EBITDA will depend on cost structure and allocation methodology.

Subscribe to our newsletter!

Get the latest industry insights and market updates from CAM Advisors.